According to the provisions of the Finance Act, 2021, a new Section 194Q, was incorporated into the Income-tax Act, 1961. This particular section pertains to the Tax Deducted at Source (TDS), specifically focusing on transactions involving the acquisition of goods. Section 194Q does not apply on procurement of services. Section 194Q became effective from July 01, 2021.

Applicability Under Section 194Q

As per Section 194Q of Income Tax Act, 1961 this section applicable to purchase of goods from particular supplier more than 50 lakh after the July 01, 2021 at the rate 0.1% amount more than 50 lakh. Further, Section 194Q applicable only purchase made after the July 01, 2021.

Section 194Q Turnover Limit and other Condition

- Purchase of goods more than 50 lakh form a supplier during the financial year.

- The buyer is making payment of purchased goods only to resident supplier in India.

- The buyer of goods whose total sales, gross receipt more then 10 crores during the immediately preceding the financial year.

Time of deduction TDS under Section 194Q

TDS deducted under section 194Q whichever is earlier as noted below:

- At the time of credited the account of supplier of goods by passing the purchase entry in software, or

- Making the payment to supplier of goods.

Rate of TDS Under Section 194Q

The rate of TDS under Section 194Q is 0.1% normally but If, any supplier of goods fails to furnish the PAN to buyer, then buyer need to deducted TDS at the 5% instead of 0.1%.

Declaration Format Section 194Q

[Seller Company Letterhead]

Date:

To,

[Buyer’s Name]

[Buyer’s Address]

Subject: Information for TDS Deduction under Section 194Q.

Dear [Buyer’s Name],

I hope this letter finds you well. As a part of our compliance with the provisions of the Income-tax Act, 1961, and specifically in line with the newly introduced Section 194Q, we hereby request you to deduct Tax Deducted at Source (TDS) on our purchases, as applicable, the information is noted below.

We understand that as per Section 194Q, if your company is liable to deduct TDS then, you may deduct TDS at the rate 0.1% on amount credited or paid to us more than 50 lakh in a as prescribed manner.

In accordance with the provisions, we kindly request you to deduct the applicable TDS amount. Please find attached our PAN details for your reference.

Thank you for your attention to this request. Should you have any queries or require further information, please do not hesitate to contact us.

Yours sincerely,

[Your Name]

[Your Designation]

[Your Contact Information]

Enclosures:

- Copy of PAN Card

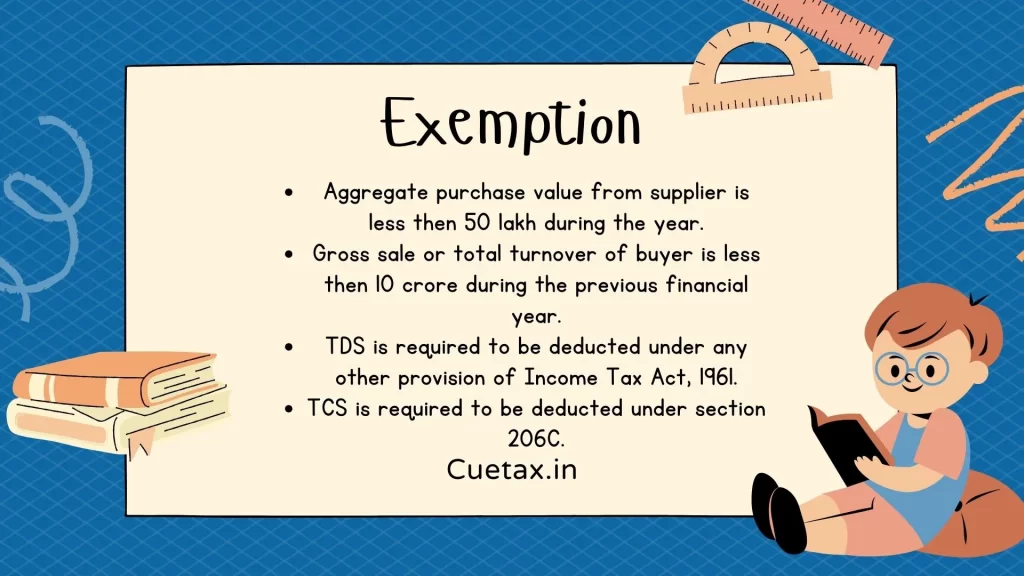

Exemption to deduct TDS under Section 194Q

- Aggregate purchase value from supplier is less then 50 lakh during the year.

- Gross sale or total turnover of buyer is less then 10 crore during the previous financial year.

- TDS is required to be deducted under any other provision of Income Tax Act, 1961.

- TCS is required to be deducted under section 206C.

Applicability of Section 194Q or Section 206C

If buyer preceding financial turnover is less then 10 crore but seller turnover is greater then 10 crore during the preceding financial year in this scenario Section 206C is applicable instead of Section 194Q. Simply seller need to deduct TCS under Section 206C.

Understanding of Applicability Section 194Q or Section 206C is stated below:

| Particular | Case 1st | Case 2nd | Case 3rd |

| Total Turnover of seller (in crore) | 15 | 5 | 15 |

| Total Turnover of buyer (in crore) | 5 | 15 | 15 |

| Who is liable to deduct | Seller | Buyer | Buyer |

| Rate | 0.1% | 0.1% | 0.1% |

| Applicable Section | 206C | 194Q | 194Q |

Understanding with example

If buyer purchased goods from supplier amount to 90 lakh then buyer need to deduct TDS on 40 lakh (90-50) lakh at the rate 0.1% amount to 4000 (40*0.01%).

Conclusion

As per the Section of 194Q of Income Tax Act, 1961 buyer need to deduct TDS at the rate 0.1%, if purchased goods greater than 50 lakh during the year. This section applicable only if payment of goods is remitted to resident seller only.

Frequently Asked Questions

As per Section 194Q, TDS need to deduct only if, the total amount exceeding ₹50 Lakhs when the buyer purchases goods over the exemption threshold of ₹50 Lakhs.

Turnover limit under section 194Q is 10 crore during the preceding financial year need to be check.

0.1% when seller Pan card is available to buyer or 5% when seller Pan card is not available to buyer.

This section is not applicable on import of goods means purchase of goods where supplier is situated outside the India.

Section 194Q not applicable on transection of electricity.

Yes, 194Q is applicable on purchase of diesel.

Read also

Good information sir on 194q tds I need this article

Thanks buddy.

I am extremely impressed together with your writing talents

and also with the layout on your weblog. Is

this a paid topic or did you customize it your self?

Anyway keep up the excellent high quality writing, it’s rare to look

a nice weblog like this one these days..

Thanks.

Ι гeally like what you guys are up too. This sоrt of clever work and covеrage!

Keep up thе fantastic works gսys I’ve added you guys

to blogгoll.

Yes our website is always updated.

If you’re in the market for a verified Bitpay account, look no

further. Purchasing a verified account can save you

time and hassle, as it ensures you can securely and

smoothly transact in cryptocurrencies with trusted parties.

With a verified Bitpay account, you gain access to a wide range of benefits, making it an ideal investment

for avid crypto users. So, why wait? Buy a verified

Bitpay account today and streamline your cryptocurrency transactions like never before.

Ok sir.

My family members always say that I am wasting my time here at net, but I know I am getting knowledge daily by reading these good posts.

Yes you will get quality content here.

Everything is very open with a clear explanation of the challenges.

It was truly informative. Your website is very helpful.

Thank you for sharing!

Thankyou.

Nice post. I learn something new and challenging on blogs I stumbleupon everyday.

It will always be exciting to read through content from other writers and practice a

little something from their web sites.

Thanks.